Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur.

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur.

Full HR & Payroll coverage for Philippines, Singapore, Malaysia, Hong Kong, and Indonesia. Each market has local support teams and built-in compliance features.

How does pricing work as we scale?

Starting at $3/employee/month for core features. Volume-based discounts are available for growing teams. Book a demo for custom pricing.

How do you handle security?

Enterprise-grade security with ISO 27001, GDPR certifications, and local data residency options.

How long is implementation?

4 weeks average. Includes free data migration, setup, and team training. No hidden fees.

What makes Omni different from global HR platforms?

Built specifically for Asia with local payroll processing, same-day support in Asia time zones, and 40% lower cost than global alternatives.

Download this resource and access it anytime, anywhere.

*By submitting your details, you hereby agree to our Terms & Conditions and Privacy Policy . Yoy may always opt-out from our mailing lists in accordance with the privacy policy

Summary. India's Income Tax Act 2025 came into force on 1 April 2026, replacing a law that had been in place for decades. For HR and payroll teams, the changes are immediate — revised perquisite ceilings, an expanded HRA metro city list, new form numbers, and updated PAN thresholds all need to be reflected in the first payroll run of FY 2026–27. The income tax changes in Budget 2026 add further updates to TCS rates and capital gains treatment. Income tax slabs remain unchanged. This guide breaks down every change, which instrument it comes from, and exactly what HR teams need to action.

See OmniHR in action

Schedule a personalized demo today to see how we help mid- market teams.

India is set to see several income tax changes taking effect from 1 April 2026 onwards for FY2026-2027. These include the introduction of the Income Tax Act 2025, the Tax Year concept, revised ITR filing deadlines, and more.

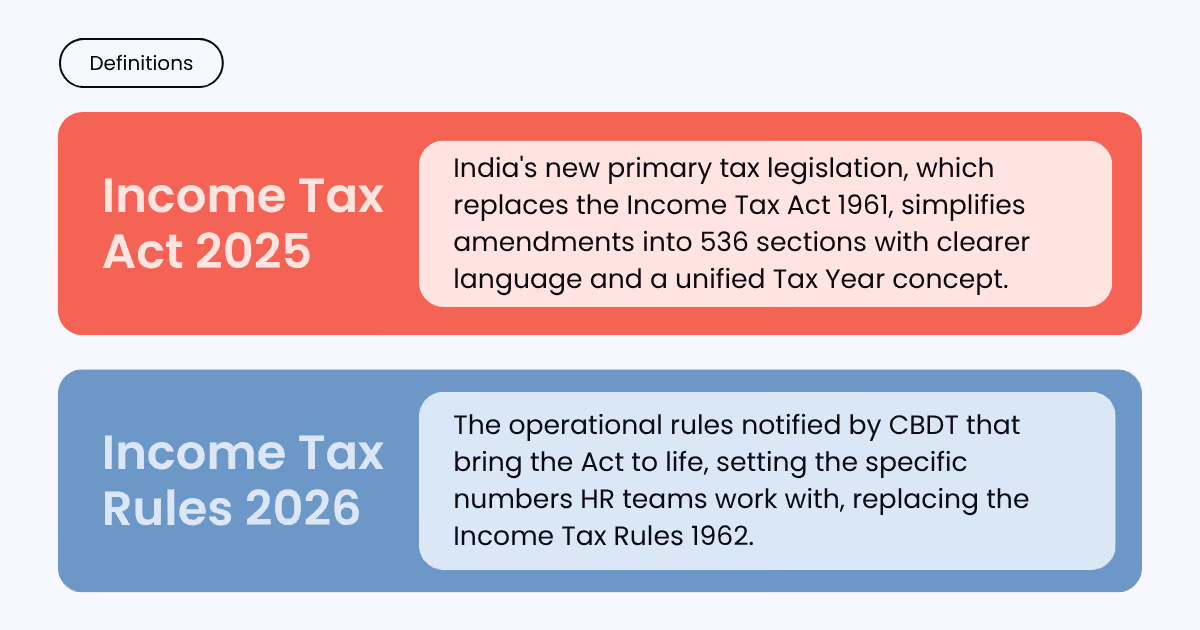

Understanding the Income Tax Act and Rules

Before we get into the specific changes, it helps to understand what these two instruments are and how they relate to each other.

Category

Income Tax Act 2025

Income Tax Rules 2026

Instrument type

Primary legislation

Subordinate rules (CBDT notification)

Passed / Notified

21 August 2025

Notified March 2026

In effect from

1 April 2026

1 April 2026

Sets

Legal framework structure, ‘Tax Year’ concept

Specific monetary limits, forms, PAN thresholds, perquisite values

HR relevance

Terminology updates, structural changes

Payroll computations, declarations, and forms

Important: Income tax slabs and rates remain unchanged for FY 2026-27. The reforms are mainly structural and procedural, not a tax hike. The focus is on simplification, transparency, and inflation-adjusted allowances.

Income Tax Act 2025

The Income Tax Act 2025 is a complete replacement of the Income Tax Act 1961. The new Act was passed by Parliament and received Presidential assent on 21 August 2025. It came into force on 1 April 2026.

Throughout the decades, the Income Tax Act 1961 had become unwieldy with continuous amendments, complex cross-references, and outdated language. The new Income Tax Act 2025 addresses all these with a cleaner, leaner structure.

Key features of the Income Tax Act 2025:

Replaced the Income Tax Act 1961 in its entirety

Reduces total sections from 800 to 536

Introduces the unified ‘Tax Year’ concept, removing the Previous Year / Assessment Year distinction

Uses plain language to reduce ambiguity and litigation

Introduces digital-first, faceless assessment procedures to reduce human interface

Retains existing tax rates, slabs, and most substantive provisions unchanged

Existing PAN, TAN, assessments, and prior-year filings remain fully valid

Income Tax Rules 2026

A set of new tax rules notified by the Central Board of Direct Taxes (CBDT) that operationalise the Income Tax Act. These new tax rules came into effect on 1 April 2026 and replace the Income Tax Rules 1962.

While the Income Tax Act sets the legal framework, the Income Tax Rules set the specific numbers, such as the monetary ceilings for perquisites, the PAN thresholds, the form numbers, and the HRA city classifications. These are the changes that directly impact HR and payroll teams, and must be reflected in salary structures, declaration forms, and tax computations moving forward.

Key features of the Income Tax Rules 2026:

Reduces total rules from 511 to 333

Reduces total forms from 399 to 190 through consolidation and renumbering

Update monetary limits for perquisites and allowances to reflect current market rates and inflation.

Expands the list of metro cities for HRA purposes

Revises PAN quoting thresholds across high-value transactions

1. The ‘Tax Year’ Concept

One of the most fundamental structural changes in the Income Tax Act 2025 is the replacement of the Previous Year / Assessment Year framework with a single, unified concept: the Tax Year.

This means:

Income earned from 1 April 2026 to 31 March 2027 fails under Tax Year 2026-27.

No more translating between two frames when you are completing declarations or filing income tax returns.

All statutory language in the Income Tax Act 2025 uses ‘Tax Year’ moving forward

Note: Tax Year is aligned with the Financial Year - so no change to accounting periods is required.

HR Action: Update all internal HR documents, payroll software labels, employment contract templates, and communications to replace ‘Previous Year / Assessment Year’ with ‘Tax Year’

2. Revised Perquisite Valuations

Under the new Income Tax Rules 2026, the monetary thresholds for employer-provided perquisites have been revised. These changes directly affect the taxable components in employees’ salary calculations and Form 130 (TDS certificate).

Note: These revised limits apply under the old tax regime only. Employees under the new tax regime do not receive these exemptions.

Perquisite

Old Limit

New Limit (FY 2026–27)

Children’s Education Allowance

₹100/month per child

₹3,000/month per child

Hostel Expenditure Allowance

₹300/month per child

₹9,000/month per child

Employer-Provided Meals

₹50 per meal

₹200 per meal

Non-Cash Corporate Gifts

₹5,000/year

₹15,000/year

Company Car – Engine up to 1.6L

₹1,800 + ₹900/month (driver)

₹8,000 + ₹3,000/month (driver)

Company Car – Engine above 1.6L

₹2,400 + ₹900/month (driver)

₹10,000 + ₹3,000/month (driver)

Employer Loan Exemption (Medical)

Up to ₹20,000

Up to ₹2 lakh

Overseas Medical Treatment (Income Cap)

Income below ₹2 lakh

Income below ₹8 lakh

Key perquisites notes for HR teams:

Home-to-office commute is no longer a perquisite - remove from payroll calculations entirely.

Employer loan perquisite: different between the SBI lending rate and the actual rate charged to the employee.

Loans up to ₹ 2 lakh and loans for medical emergencies are fully exempt.

The children’s education allowance has risen 30-fold - proactively communicate this to employees as it materially affects take-home pay under the old regime.

3. HRA Metro City Expansion

The Income Tax Rules 2026 expand the metro city list for House Rent Allowance exemption, lifting four cities from 40% to 50% of salary exemption. This is one of the most impactful changes for large portions of the salaried workforce in tech and finance hubs.

City

Previous Rate

New Rate (FY 2026–27)

Status

Mumbai

50% of salary

50% of salary

Unchanged

Delhi

50% of salary

50% of salary

Unchanged

Kolkata

50% of salary

50% of salary

Unchanged

Chennai

50% of salary

50% of salary

Unchanged

Bengaluru

40% of salary

50% of salary

New - added in 2026

Hyderabad

40% of salary

50% of salary

New - added in 2026

Pune

40% of salary

50% of salary

New - added in 2026

Ahmedabad

40% of salary

50% of salary

New - added in 2026

HRA rules that have NOT changed:

The three-way minimum formula remains unchanged.

Exemption = lowest of actual HRA received (40/50% of salary), or rent paid minus 10% of salary

All cities outside these 8 remain at 40% exemption

Applies under the old tax regime only

HR Action: Employees in the newly added areas, such as Bengaluru, Hyderabad, Pune, and Ahmedabad, should resubmit Form 124 to apply the correct 50% HRA exemption. Also, be sure to update Form 124 templates to include a mandatory relationship disclosure field for rent paid to parents or spouse.

4. New Tax Forms

Under the Income Tax Act 2025, the new tax rules reduce the total number of forms. All new form numbers are effective from 1 April 2026; payroll systems and declaration templates must be updated before the first payroll run of FY 2026-27.

Old Form

New Form

Purpose

Form 16

Form 140

TDS certificate for salary and pension income

Form 12BB

Form 124

Employee investment and rent declaration (includes new relationship disclosure field)

Note: The consolidation of four TDS forms into a single Form 141 reduces compliance burden for property-related TDS. Form 168 (replacing Form 26AS) will not display the Aadhaar number, reinforcing PAN-based identification.

5. ITR Filing Deadlines and Compliance Relief

The Finance Bill 2026 extends several key filing deadlines and introduces a more flexible revised return window.

Item

Old Deadline

New Deadline

Notes

ITR-3 / ITR-4 (Non-audit)

31 July

31 August

Extended for salaried and non-audit business filers

Salaried / Individual ITR

31 July

31 July

Unchanged

Audit cases

31 October

31 October

Unchanged

Revised return

31 December

31 March of the following year

Fee applies for filing after 31 December

Global teams must identify all employees with overseas income or foreign assignments.

A one-time 6-month relaxation applies for employees with global income reporting obligations during the transition to the new Act.

Employees who file revised returns after 31 December will be subject to a nominal late fee.

6. Updated PAN Requirements

The income tax changes in Budget 2026 also revised mandatory PAN quoting thresholds across several transaction types. The focus is on rationalization and stronger digital enforcement rather than introducing new compliance requirements.

₹10 lakh (non-cash) or ₹1 lakh (cash) - reported to the tax department

HR Action: For company car schemes, PAN must now be quoted for vehicles above ₹ 5 lakh (not ₹ 10 lakh under old rules). This covers virtually all company vehicles. Align fleet procurement and HR operations teams before approving new vehicle requests.

7. TCS Rationalization

Budget 2026 tax updates rationalized TCS (Tax Collected at Source) rates, providing relief for employees making overseas remittances under the Liberalized Remittance Scheme (LRS).

Category

Old TCS Rate

New TCS Rate

Notes

LRS - Education and medical remittances

5% (above ₹7 lakh)

2% (flat, no threshold)

Relief for overseas education loans and medical treatment

Overseas tour packages

5% or 20% (dual rate)

2% (flat)

Simplified single rate applies to company travel arrangements

LRS - Alcoholic drinks

1%

2%

Increased

All other LRS / applicable categories

Varied

5% (flat)

Rationalized broad rate

8. Investment & Capital Gains Changes

These Finance Bill 2026 changes are relevant to HR teams managing ESOPs, RSUs, share buyback schemes, or executive compensation plans.

Category

Old Treatment

New Treatment (from April 2026)

Share buybacks

Taxed as deemed dividend at slab rates

Taxed as Capital Gains in shareholders’ hands

Interest on loan against shares

Deductible against dividend income

No longer deductible against dividend income or mutual fund income

TDS on NRI property purchases

Mandatory TAN + 20% TDS

Use buyer’s PAN; TAN no longer required

STT - F&O (options)

0.0625% (sell side)

0.15% (revised upward)

Note on ESOP / buyback plans: The shift from dividend to capital gains treatment for buybacks may affect the tax efficiency of executive liquidity arrangements. Compensation teams should review affected plans with a credible tax advisor to ensure compliance with the new tax rules.

Your HR Action Checklist

Update payroll software to generate Form 130 (replacing Form 16) and Form 168 (replacing Form 26AS).

Replace Form 12BB with Form 124 in all declaration workflows. Add a relationship disclosure field for rent to the parent or spouse.

Consolidate TDS forms 26QB / 26 QC / 26QD / 26QE into Form 141.

Apply 50% HRA exemption for employees in Bengaluru, Hyderabad, Pune, and Ahmedabad for the old tax regime only.

Revise perquisite ceilings in payroll as per the new tax rules.

Remove home-to-office commute from perquisite calculations entirely.

Update PAN compliance threshold for company car procurement to ₹ 5 lakh (revised down from the old tax rules).

Brief the global team on the 6-month overseas income transition window.

Update all HR communications to use ‘Tax Year’ terminology under the Income Tax Act 2025.

Communicate revised return deadline change to employees: now extendable to 31 March of the following year, with a late fee after 31 December.

Review ESOP / share buyback plans against the new capital gains treatment under the Budget 2026 tax updates.

Stay Compliant with India’s New Income Tax Act From Day One

India’s income tax changes in Budget 2026 and new tax rules are broad, layered, and extremely time-sensitive.

Between the structural overhaul of the Income Tax Act 2025, the revised perquisite and HRA rules in the Income Tax Rules 2026, and the TCS and capital gains treatment from Budget 2026, HR teams find themselves navigating three separate instruments, all within a tight timeline.

Getting the details right is crucial as incorrect perquisite values, outdated form numbers, or the wrong HRA metro city classification not just creates compliance risk, it also affects employee take-home pay and trust.

Omni’s managed payroll service for India takes the complexity out of the equation. Here’s what's included:

Monthly payroll calculations compliant with statutory requirements, bank file preparation, and payslip distribution via email and our employee self-service portal.

Monthly submission of Provident Fund and ESI contributions, plus professional tax deduction statements.

Annual income tax declaration releases, year-end investment proof validation, and tax recomputation for employees.

Quarterly ETDS return filing on the TRACES portal and Form 16 issuance.

Ready to simplify India Payroll? Book your product tour with our team today and learn more!

Frequently Asked Questions

1. Which cities are now considered metro cities for HRA exemption?

The 8 metro cities under the Income Tax Rules 2026 are Mumbai, Delhi, Kolkata, Chennai, Bengaluru, Hyderabad, Pune, and Ahmedabad. All these cities are qualified for a 50% of salary HRA exemption. All other cities remain at 40%. This applies under the old tax regime only.

2. Has the HRA exemption formula changed?

No. Only the metro city list has expanded. The exemption remains the lowest of:

Actual HRA received or

Rent paid minus 10% of salary

3. What are the revised perquisite limits under the Income Tax Rules 2026?

Children’s Education Allowance: ₹ 3,000/month per child

Hostel Allowance: ₹ 9,000/month per child

Meal Vouchers: ₹ 200 per meal

Non-Cash Corporate Gifts: ₹ 15,000/year

Company car up to 1.6L: ₹ 8,000/month + ₹ 3,000 driver

Company car above 1.6L: ₹ 10,000/month + ₹ 3,000 driver

Home-to-office commute: removed as a perquisite entirely

All revised limits apply under the old tax regime only.

4. What replaces Form 16 and Form 12BB?

Form 130: Replaces Form 16 as the TDS certificate for salary income

Form 124: Replaces Form 12BB for employee investment and rent declarations

Form 141: Consolidates TDS forms 26QB-26QE

Form 168: Replaces Form 26AS as the annual tax credit statement

All changes are under the Income Tax Act 2025 and Income Tax Rules 2026, effective 1 April 2026.

5. Have income tax slabs changed for FY 2026-27?

No. Income tax slabs remain unchanged under the income tax changes in Budget 2026 for FY 2026-27. The Income Tax Act 2025 specifically retains the existing rate structure.

The budget 2026 tax updates focus on structural changes, perquisite valuations, HRA expansion, new forms, and compliance timelines, rather than rate slabs.

6. What is the new ITR filing deadline for non-audit filers?

Under the new tax rules, it is extended to 31 August for ITR-3 or ITR-4 non-audit cases. Salaried individuals still file by 31 July. Revised returns can now be filed until 31 March of the following year, though a nominal fee applies for filings after 31 December.

7. What are the updated PAN thresholds under the Income Tax Rules 2026?

Cash deposits/withdrawals: PAN required if total exceeds ₹ 10 lakh/year

8. How has TCS changed for LRS remittances under Budget 2026?

LRS for education and medical treatment: flat rate 2% TCS

Overseas tour packages: flat rate 2% TCS

All other LRS categories: flat rate 5% TCS

9. How are share buybacks treated under Budget 2026 tax updates?

Buyback proceeds are now treated as capital gains in the shareholders’ hands under the Finance Bill 2026, replacing the earlier treatment as deemed dividends. This is important for RSOP and executive compensation plans using buyback liquidity.

Additionally, interest on loans taken to invest in shares is no longer deductible against dividend or mutual fund income.

10. Do the new perquisite limits apply under the new tax regime?

No. The revised perquisite limits and allowance exemptions under the Income Tax Rules 2026 apply exclusively under the old tax regime. Employees who have opted for the new tax regime do not benefit from these revised ceilings and should be advised accordingly during annual income tax declarations.

Frequently Asked Questions

No items found.

Future-proof your leadership bench.

Stop guessing who is ready for promotion. Use OmniHR to identify, nurture, and retain your top performers with data-driven succession planning.

Download this resource and access it anytime, anywhere.

*By submitting your details, you hereby agree to our Terms & Conditions and Privacy Policy . Yoy may always opt-out from our mailing lists in accordance with the privacy policy

.avif)

.avif)

.avif)